rpllib

-

Posts

66 -

Joined

-

Last visited

-

Days Won

20

1 Follower

Recent Profile Visitors

4,731 profile views

rpllib's Achievements

")

-

'HE WAS AN ABSOLUTE ACE' ‘HE WAS THE MOST OPEN AND ENGAGED SHOP OWNER I EVER WORKED WITH’ "He was a great guy, and he's going to really be missed" This is what they will say about you when your gone. All statements spoken and written about shop owners in the last 6 weeks. All younger than me. I am 64 This doesn't sound like retirement to me. Take the time to live while your vertical. "TIME" is the only currency that really matters, Imo.

-

A year and a half ago, my lead tech, in his early 50's), came to me and said he was done, after 30 years with us. He had an especially frustrating few weeks with diags that did not go well. He knew he couldn't quit working, as he has young children still at home, but he was going to find something less frustrating, even if it meant taking a big pay cut. He had already discussed it with his wife, and they were in agreement that they would do whatever was necessary to get him out of this industry, that he felt he was too old to manage any longer. I could tell he did not want to quit, he could just not see any way out of this frustrating situation. We made a few small changes, one of which was to implement 1 hour virtual(mostly) or live(occasionally) training sessions weekly, with all techs, grouped by primary job duties. I see this as a retention and growth tool. If nothing else, it puts the owner in front of them weekly to discuss any variety of opportunities/challenges, and provides them an opportunity to express concerns in an open environment without front counter involvement, well training on actual challenges we are seeing in our shop. It serves to help me understand the difference between what my techs want and what my leadership wants from them. Here is some data regarding this thought, that came across my desk recently: Essentially the survey discussed in the article shows what aspect of employment managers believe is important to staff, and then the comparison of that list, to what 396,000 employees answered as most important to them The answers given by managers were ranked as: Good wages Good benefits Job security Promotion opportunities Good working conditions Ample time off for personal reasons Good training Appreciation of work Sympathetic help/leniency for personal problems Effective leadership VS. the following answers have been given by 396,000 employees who have taken SESCO’s Employee/Management Satisfaction Survey: Appreciation for work done Feeling “in” on things Fairness/no favoritism Job security Good benefits Good wages Promotion and growth opportunities Good working conditions Effective communications Sympathetic assistance on personal problems/flexibility There is probably lessons for many of us here. Me for sure. sescomgt.com/sesco-report

- 2 replies

-

- 1

-

-

- training

- tech training

- (and 2 more)

-

The Pros & Cons of Offering Financing

rpllib replied to Joe Marconi's topic in Credit Cards, Payments, Financing

Here are my cliff notes from last weeks leadership meeting with my front counter staff: the incredible importance of offering financing, all the time, and especially in times like this if your concerned prices are getting out of hand, offering financing to offset even folks that have the money will consider financing, "until things cool off" maybe no better time to offer financing to those that don't need it. folks that don't need financing will not let financed accounts go past free period, but still appreciate Our shop is in a area where the average household operates closer to their "breakeven" point for household expenses, than many. Any bad news typically effects us earlier then markets with more affluent households. Traffic was off by 11% in April and sales by 24%, after a record 24 month period right up thru the end of the first first quarter 2022. We tend to attract the "higher" income households in our market, and rarely have any kind of "payment" issues. If I compare my financial diligence and attitude that i practiced in my lifetime, to those households, then I believe that those customers that can afford repairs, may still be interested in financing with free periods as a cushion, against uncertain times. I have used hundreds of thousands of dollars in "free money" financing over my lifetime very effectively, without accruing interest charges, even though I could have paid for most of those dollars, for most of my life. If you are worried about driving your customers into higher debt, then make sure you are putting your extended financing in the hands of the ones that don't need it, not concentrating on the ones that do, or only offering as a last resort. We use Synchrony Card for as many as can be approved for it, which offers 6 months interest free. This is most of our financing. We brought in Easy Pay, for those that can't be approved for tier one credit. I still believe it can be used effectively for those with credit issues, and comes with 90 days interest free. We strongly encourage payoffs within the free period. We run 6-8% of sales that are financed, average throughout the year, with tire season months running 15-20%. I would like to see the average in the 15%-20% range for the year. Right now, maybe more than any time in my business career, I believe we have the best opportunity to offer free money to those that don't need it, but would appreciate it. % financed, is now a monthly metric that we track and discuss weekly. -

I wonder if anyone would like to throw some ideas at this list. We are 18 months away and it seems like we should get it in gear. Thank You 1. SELLER Prepare letters to advise vendors and that SELLER no longer responsible for accounts after sale date, 30 days prior 2. SELLER prepare letters to receivable customers, joint letter with BUYER most likely 3. Dissolve Seller corporation or what? As of sale date? 4. SELLER work on list of todo’s under Other Considerations, below 5. BUYER creates new corporation and sets up new vendor accounts 6. BUYER get sales tax license, set up federal id, corporation if desired, what else?? -- 7. Seller cancel SMS, BUYER establish shop management system, change names, DBA’s as necessary, so printouts are correct 8. Seller cancel all subscriptions in sellers name and BUYER establish those relationships and create accounts as desired 9. BUYER prepare letters to vendors and receivable customers 10. Wind down receivable customers as much as possible, 90 days prior to sale date 11. Seller contact business insurance and health insurance carriers 90 days in advance to see what is required to cancel insurances. 12. SELLER transfer phone numbers to BUYERS account with phone company. 13. ????? This seems like just the start Other considerations: Meet with your board, partners, or members to pass a resolution to formally dissolve the business. Notify the IRS within 30 days of dissolution, using Form 966. File articles of dissolution with the state where your business was formed and any other state where it is registered. Notify contacts for all contracts that are being assigned to or assumed by the buyer. Notify creditors to explain how bills will be paid, either by you or by the buyer. Cancel business permits or licenses, assumed business names, and other registrations. Cancel insurance policies Pay off bills and collect accounts receivable Distribute assets remaining in your business after the sale closing, to shareholders, partners or members the business is a corporation or LLC. Close your employer ID number with the IRS. Close business bank accounts and credit cards. Close business line of credit, if any. Pay final wages to employees, and payroll taxes and fees due to tax authorities. File necessary tax forms, using the IRS “Closing a Business Checklist”

-

"but the proceeds from the sale of your business may not be enough to financially support you into retirement" If you are a shop owner in your 30's or 40's, I hope you listen well to Joe's words. My wife and I worked most of the first 30 years in our business with less then $100k in owner salaries, wages, perks, discretionary spending, ect. Much of that time I was not even sure we would survive as a viable entity till our retirement, so saving was not an option, we considered it crucial to having any chance at life after the business. Now that we are in our sixties, have no debt, own the real estate and still managed to have a 7 figure retirement account, with only minimal family wealth as part of that figure, we feel we are in the best position of all. For me, that position is the opportunity to chose good health and freedom of choice in what we do on a daily basis, over stressing about having to sell the business, to have a life. The most liberating part of the whole thing, is the knowledge that even if we chose liquidation as our viable exit plan, we would be just fine. Even if the building had to lay empty for a few years, we will be just fine, even if we had to sell 350k of non real estate business assets for 50k, we will be just fine. Even if we got nothing out of the business/assets at all, and the real estate went back for delinquent property taxes, even then we would be just fine. I believe many can accomplish the same/similar to us, or better, if you have a plan and work the plan from the youngest age you can. Thank You Joe, wise words

- 25 replies

-

- 2

-

-

- exit plan

- exit strategy

- (and 1 more)

-

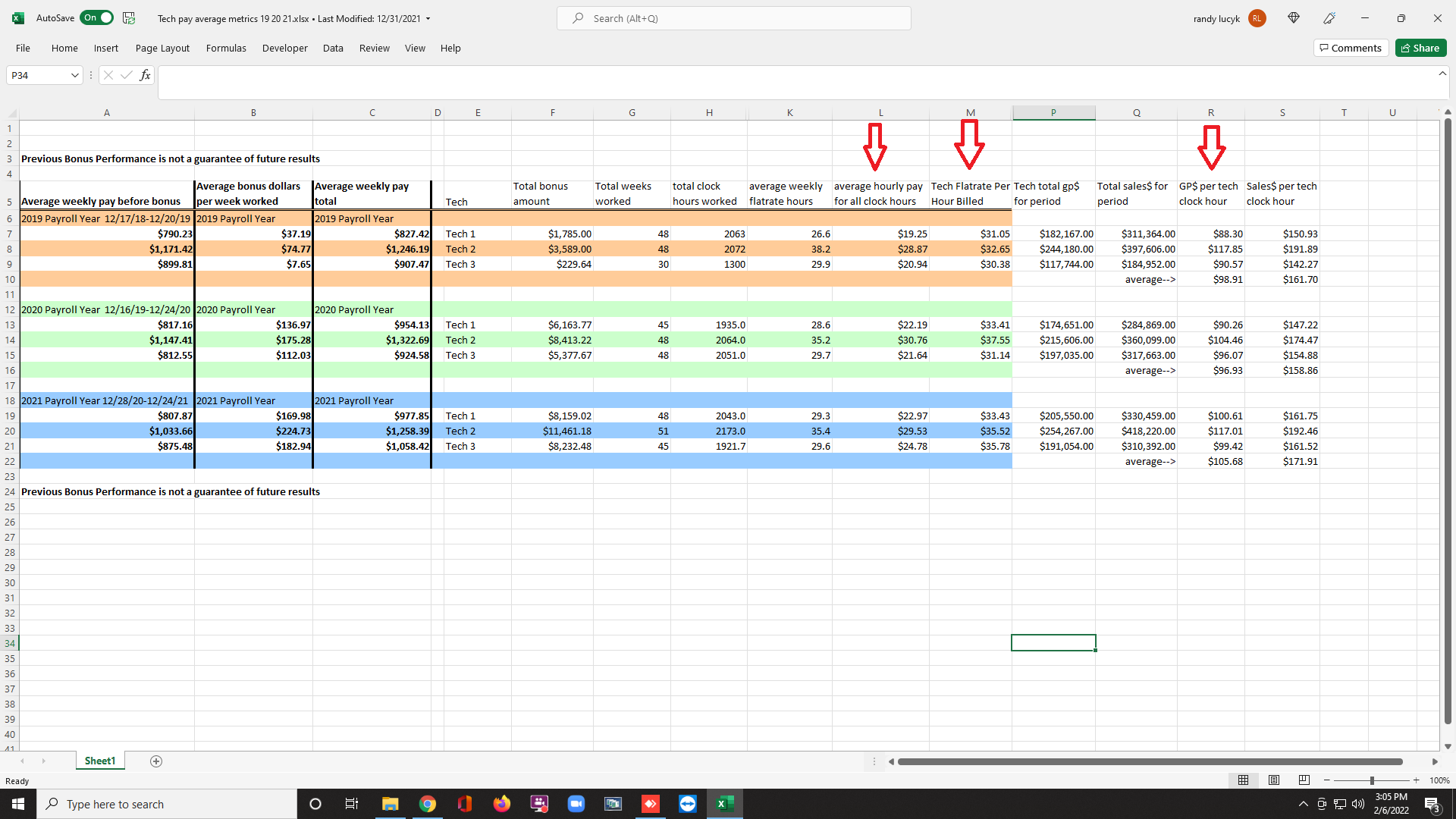

We have a pop graph in our SMS that we have set profitability goals on, so it is easy to look at profitability on a invoice basis. This assumes that you regularly update your cost of labor in your Sms, which we do, and that you are razor sharp on costing parts accurately. Technician Hourly Pay (total pay / hours worked) This is not tech hourly pay, if you pay hourly. This figure does not care how you pay on a week to week basis. It is total W2 wage "gross dollars" (paid in a period) to the tech divided by total hours worked in clock time (in the same period). This does count on accurate time records, but it does not care how the gross pay is accumulated. Technician Effective Flat Rate (total pay / billed hours). This is correct, It is total W2 wage "gross dollars" (paid in a period) to the tech divided by total hours "billed" in labor time (in the same period). Gross Profit per Technician Clock Hour (GP / hours worked). This is correct. Accurate total GP$ generated by a technicians activities for a specific time period, divided by total clock hours worked in the same time period. The effort is aimed at trying to come up with some financial benchmarks, that are not affected by type of pay plan. We have techs on 2 different types of pay plans. "So far, I've focused on startup survival over efficiency. We are just now starting to look deeper and wider" sounds like you are on the right track. I hope you are quicker then I am at picking up on this kind of stuff. I am 42 years in Jobs that span multiple days are accounted for on the day they are closed. It catches up over the course of weeks and month. I meet with my staff in groups (leadership, service techs, lube and tire techs)weekly, and the first 10 minutes is going over month to date goals and performance. We were guilty of what Jeremy describes in the video, for most of my career. We would get to the end of the month, and look back, and say "while that month sucked". Now, our daily trackers play as a slide show on our screen savers (a dozen workstations in the shop and growing), as well as staying focused with the weekly meetings. It helps a lot, maybe more than any of us realize, if you are "digitally adept" when it comes to things like computers, networks, software, ect. Excel has been our close friend for decades

-

I am a very big believer in what Jeremy is describing. The first attachment is my service techs performance for the past three years. I have always wondered how we do against shops in a similar business model and retail environment, especially on the items marked with red arrows. The second attachment is what my techs fill out every day. The orange arrows are what they fill in daily, using two SMS reports. The rest populates based on those 4 columns. We would fit somewhere between "Generalists" and "General Generalists", in the descriptions below. Specialized Specialists Approx 70% or more of service dollars come from work on only certain aspects of automotive service, examples might be: Diag specialists Locksmiths Hvac specialists Electrical specialists Transmission specialists Brake Specialists Adas specialists Specialized vehicles(fire, rescue, motorhome, ect) Oil change Average Opportunity for technicians working at shops in this category, to see similar issues and perform similar services on a repeating basis – High Likelihood Specialists Approx 70% or more of service dollars come from work on only one or two brands of vehicles Average Opportunity for technicians working at shops in this category, to see similar issues and perform similar services on a repeating basis –Highest Likelihood General specialists Approx 70% or more of service dollars come from work typically only on cars from a certain part of the world, like euro or asian, or a specific range of services. Average Opportunity for technicians working at shops in this category, to see similar issues and perform similar services on a repeating basis –High Likelihood Generalists Most of the automotive service facilities fit here. Most makes and models, most services. Average Opportunity for technicians working at shops in this category, to see similar issues and perform similar services on a repeating basis –Low Likelihood General Generalists These will typically be small market generalists. (approx. <10k households in a 10 mile radius, or < 30 homes per sq. mile in a 10 mile radius) There would typically be no specialists, beside oil change, in these markets, so these shops will likely have a broader service offering,. May include mix of light, medium and heavy duty vehicles and/or specialized vehicle service like fire, rescue, motorhomes, ect. Average Opportunity for technicians working at shops in this category, to see similar issues and perform similar services on a repeating basis –Lowest Likelihood

-

About ready to hang it up.

rpllib replied to tirengolf's topic in Exit Strategy, Retirement, Selling Your Repair Shop

If you have any internal candidates that may be the next owner, then Bob Ward could offer insight/assistance. https://www.perpetualbusiness.co/ Search on his business and name. He has a lot of resources for shop owners looking to transition If looking for an outside buyer, You would also find value in a conversation Art Blumenthal. https://art-blumenthal.com/ Again lots of great resources with a simple search. Both these guys are passionate about helping auto shop owners. I also agree with dstremski. Local commercial brokers have been successful and discrete. Best of Luck -

Isaac Looks like you have taken on a big nut. I suspect you don't have that whole building, but what ever portion you have looks impressive. I love the looks of your location! You have what appear to be nice neighborhoods around you, with a lot of newer/well kept housing. You appear to be in what I call a 20/20 market. Less than 20% of the homes in your direct market area have household incomes above 75k per year. Less than 20% of those households have bachelor level, or greater education levels. These numbers typically indicate a stronger propensity for "do it yourselfers". These "straight up demographics" of those neighborhoods does not match up to what i am seeing in Google street view. I was surprised to find such nice, well kept housing close to your location. Says a lot about quality of the individuals living in those markets. I believe you likely have more then enough "do it for me" customers in your area, you just need to work towards attracting those type customers. Our shop is in a similar market, less than 20/20. We also went thru our period of working for used car lots, thinking some work is better than none. One of the only reasons we got any of the used car business, is we were cheaper than the surrounding shops to begin with, largely unprofitable, and most lot managers would still beat us up. We only ever had one lot that was decent to work with, and when that manager changed, we got out of that business. We also don't work well with any of the extended warranty companies for the same reason. They want to also beat you up, control margins, and essentially drive you out of business. We frequently have to tell customers they are going to be responsible for 20-30% of the bill, because their extended warranty does not cover the charges. I suspect that if you had the time to accurately measure you profitability from the used car work/extended warranty work, overall you would find no cash left from those services whatsoever, although they do produce some cash flow, but I would still be looking to exit that type of business as soon as possible. I am also going to guess that your labor rate is below $100 an hour. One thing that I did not understand, for much of my early life as an owner, was that cheap prices are a very expensive form of marketing. I like your google reviews and testimonials on your website. You may find it is cheaper overall to do actual marketing to any higher income, higher educational level households/neighborhoods in your area (DIFM, do it for me customers), then it is to have lower overall prices to attract customers. My method is not as easy and requires courage, lots of courage to pull it off. You have to be able to charge, what you need to charge to first survive and then prosper, and you have to be able to hold that line with friends and relatives. It is not likely that you are in a position to offer a discount from your current prices to anyone. Technicians and staffing required to operate an automotive service facility today are just to valuable to discount to anyone, until you are long established and reasonably profitable. Better to charge what you need to, and have funds to support your family, your staff and your community, Imo. You can't do it all at once, but you can work towards it. Promote the service you offer, that I read about in your reviews and testimonials You may need to seek assistance with doing actual marketing, if you are not strong in that area. I am more than happy to be wrong about any of my assumptions stated above. Best Wishes for a bright future Randy Lucyk

-

Hiring Techs Now Impossible?

rpllib replied to Obsidian Motors's topic in Human Resources, Employees

I believe some owners have just checked out, especially if they have a stable crew that takes care of most of the day to day, the bills are being paid, the owners are getting paid, ect. Maybe no one is getting paid what it is worth, but everyone is comfortable. This is the case with my friend, but does not explain the younger owners that surround him. Techs turned business owners I suspect. Maybe even DIY owners/staff running the front counters. One of the best things I ever did was to get off the front counter. Our flat rate guide labor multiplier has varied from 15% and now at 30%. This is to insure that the guide built into our POS is at the top of the labor times when the three(or more) guides are compared. It also covers some additional time for the rust/corrosion we have to deal with in the upper northern tier. Our POS system also matrix's our labor rate up $40 (33%) over our base rate, over the first 10 hours of labor. This is to cover the lower parts GP$ that typically go along with higher labor hours. I have no doubt that customers notice how much higher we are than our competitors, but we seem to find more than enough work to keep a staff of 10 busy. I won't allow my techs to be tied up on marginally profitable work, if I have a choice. I am probably the opposite of my friend. I refuse to have nothing to show for our efforts. I may close the doors one day for being too expensive and refusing to budge, but I won't have any regrets in the process. 40 plus years in business and no debt does offer freedoms that many may not have the options for. Yet I truly believe there is always room for all shops to improve, every single year. I hope we are able to kill the acronym TLDR(too long, didn't read) in our industry. There is no room for that thought process. Better we go to GPFR (get paid for reading) Best Wishes All -

Hiring Techs Now Impossible?

rpllib replied to Obsidian Motors's topic in Human Resources, Employees

"I was thinking of this topic yesterday. I received notice from the landlord that the rent will be going up about $4 per my average monthly produced hours." Well done! I believe if every shop owner should take their fixed expense increases, and drill them down to their additional cost per billable hour. At least then, maybe owners would give themselves permission to raise their labor rate. If we know that in the past 12 months our average fixed expense cost has increased be a certain dollar amount and divide that amount by the average hours we billed in a month, and that number was $8.81, do we ask ourselves "where is the money going to come from??", or do almost all of us know the answer, and react quickly. I can assure you that "react quickly" is not the case for many owners. Frustrating conversation with a close friend just yesterday, that owns a shop in a town 30 miles from mine. Town is 3 times the size of mine and has an expressway, National Guard base, with higher household incomes and higher educated households then mine, and he runs a great shop. Great techs and front counter personal. He is like the rest of us, 2-3 weeks backed up. His labor rate is sub 3 figures by fifteen points and feels like he can't go up, because he claims the dealer is sub 3 figures by 5 points, and he can't charge as much as the dealer. He is about as likeable a guy as you will meet, and has a good relationship with most of the other auto repair shops in town. He tells me their all convinced they can't go up, because of where the dealer is at, and the fact that the big tire store in town will not go up with them. What absolutely insanity! For sure, with this group of independents, they don't understand the math, or won't take the time to to do the math. For sure they don't understand the value of doing the math. I interviewed a tech yesterday as well. Works for a large dealer group in a town 30 miles north of my friends. Double the size of my friends town and even better demographics, with a good reputation. The tech tells me their 16 points north of three figures. That's lower than my lowest rate, and 28% lower then my highest rate. I know these guys know the math. I sit with them in advisory council meetings. Their sharp as hell. What gives!! Like I said, frustrating conversations. I ask my friend what he was worried about, losing work?? He already told me he spills 8-10 phone calls a day for service and how much he is disappointing his long time customers. Apologies for the cryptic labor rate. Not sure what the rules are on using simple to read actual rates in an open forum Done venting for now -

I think it is the resolvauto.com link that shows me these are not all extended warranty type scam companies, although some are for sure. Resolve is a Bridgestone Firestone USA program and it shows up on their service websites, such as Firestone Complete Auto Care websites, Terms here: https://resolvauto.com/legal/RESOLV_terms-and-conditions_2020-12-14.pdf. Plan offerings here: https://resolvauto.com/sign-up/add-plan Not sure what demographic this might work for, as it does not eliminate repair costs, and does not appear it is a good value for most consumers, but it does show that big players are testing the waters. It does appear to be a viable business model that could generate profit dollars, based on a cursory review of the monthly charges and benefits provided.

-

Hiring Techs Now Impossible?

rpllib replied to Obsidian Motors's topic in Human Resources, Employees

Something we are trying in our rural market. 25,000 postcards to every household within 15-40 miles distance from our service facility ($7000 cost). Not everyone agreed on the message, especially where the $1000 should go. The individual we are looking for, is not out looking for a job. We have tried a similar path to yours, including no less then the avenues you are trying, with zero responses in the last 3 weeks. I am hopeful we will stir up some responses. I am confident that not every technician working in this 600 square mile block we are dropping postcards to, is satisfied with their employment situation Example attached. 74136_TRAVER_1123_McKay_102521_8.5x5.5_version2.pdf -

This is a partial list of companies trying various approach's to subscription based automotive repair and maintenance. Some claim to have advanced software to administrator and monitor the programs. I expect this is definitely part of the future automotive service landscape, especially if it gets picked up by a major player. I suspect it will take a substantial subscriber base for a successful business model to evolve. https://emp.autologiq.ca/ https://www.carholdings.ca/ https://www.90autorepairclub.com/ http://www.autotekpro.com/automotive-blog/vehicle-maintenance-service.html https://resolvauto.com/ https://myautorepaircenter.com/membership/ https://www.thecarrepairclub.com/ https://www.havenautorepair.com/Coupons/Monthly-Membership-Packages https://www.membershipauto.com/ https://www.syncron.com/news/transforming-auto-dealer-services-for-the-subscription-economy/ https://www.forevercar.com/

-

How to Compute Overtime Pay

rpllib replied to bantar's topic in Accounting, Profitability, & Payroll

Your Welcome. It is a tough concept to get your head around. I can only imagine what took place in the past, that caused these complications to become law.